Note: This is the first in a series of posts on building agentic AI workflows for high-net-worth banking. This post walks through the high-level architecture. The upcoming posts will break down each agent in detail.

I also built a working prototype in Python to demonstrate this architecture. You can find the link to the prototype here.

Now let’s get into it.

James is a retired business owner.

He sold his software company last year for $18 million.

He now wants to open a new bank account with a Canadian bank and transfer $5 million into that account.

Of that $5 million, $4 million comes from the business sale proceeds. James currently holds this money in his existing bank account. The remaining $1 million comes from crypto funds held through a crypto exchange.

He expects premium service because he is bringing millions of dollars to the bank.

So James walks into the bank branch, sits down with the relationship manager, and tells her he wants to open an account.

The relationship manager nods, takes notes, and then delivers the news.

It could take more than 40 days to open his account.

James is baffled.

More than 40 days for a bank account?

He expected a few days at most. Maybe a week if they needed to verify some documents. But more than 40 days feels ridiculous.

Something is clearly broken here.

Why does opening a bank account take so long

Banks call this process KYC, which stands for Know Your Customer.

KYC is how the bank verifies who you are, where your money came from, and whether the funds are legitimate.

For a client with a few hundred thousand dollars, the process is relatively simple. But for a client like James, who is bringing $18 million into the bank, the money laundering risk is much higher. The bank needs to dig deeper into his background and financial profile.

For James, the bank has to verify his identity, understand where the $18 million came from, confirm the business sale was real, check for crypto involvement, and screen him for PEP, sanctions, and adverse media.

The relationship manager collects this information and passes it to the compliance team for review. If something is missing, the compliance team goes back to the relationship manager, the relationship manager goes back to James, and the case returns to the queue.

That back-and-forth is where much of the time goes.

That is why the bank takes 40+ days.

This is where an agentic workflow helps

Agentic AI can automate most of the review work so that the compliance officer can make a decision much faster.

One thing to understand up front. The AI does not onboard the client or make the final decision. A compliance officer still reviews the case and decides whether to onboard the client. The AI just makes that review faster.

Agentic AI does that by breaking down a complex workflow into smaller, independent tasks. Each task gets handled by a specialized agent that focuses on one specific job. Think of an agent as a focused worker with just one clear responsibility.

But before you build an agentic workflow, you need to understand the manual process first.

Start by mapping how a client is onboarded today. What information does the relationship manager collect? Which teams touch the case? Where does it get stuck? Which decisions are rules-based and which need human judgment?

Once you map the manual process, the design becomes clear. Some steps should be rules-based. Some should use existing bank systems. Some should use AI to organize messy documents. Some should remain with compliance officers who make the final judgment calls.

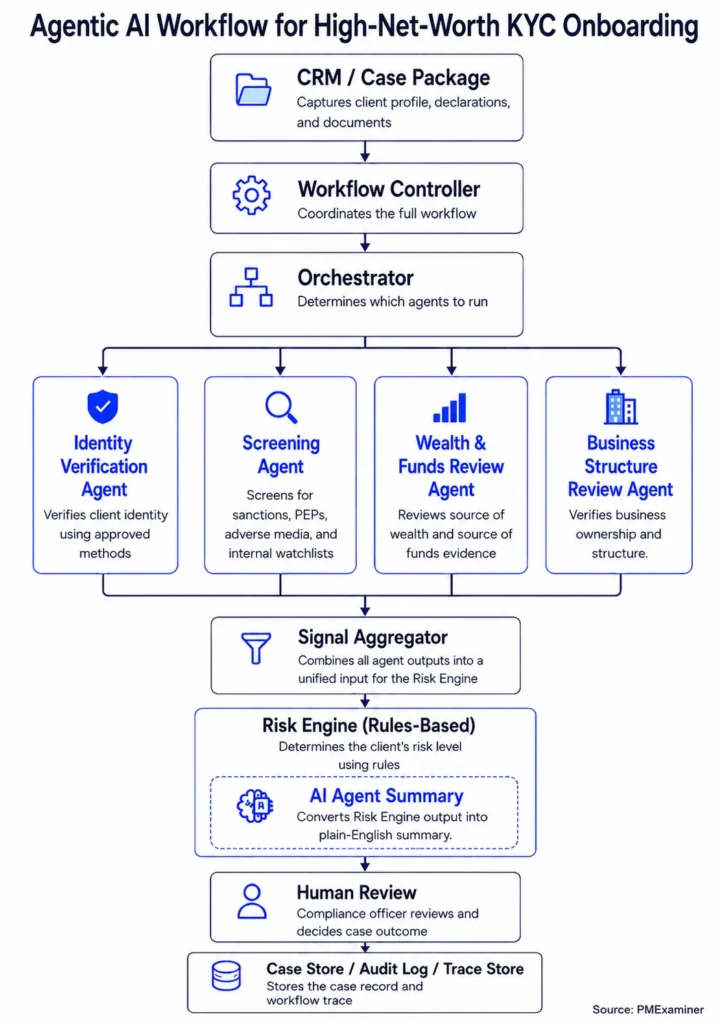

Here’s how the agentic workflow is structured

Here’s what each step does.

For simplicity, I’ll use ‘agent’ for each focused step in the workflow. When a step uses a large language model, I’ll call it an ‘AI agent.’

- The CRM is where the relationship manager enters James’s information and uploads his documents. This creates a case package, which bundles all the client information and supporting documents together.

- The Workflow Controller keeps the case moving. It starts the workflow, pauses when information is missing, resumes when the issue is resolved, and records key updates.

- The Orchestrator looks at the case and decides which agents are needed. For James’s case, it sees a business sale, crypto holdings, and high-net-worth status, so it triggers four specialist agents to run in parallel.

- The Identity Verification Agent verifies James’s identity using the bank’s approved identity verification systems.

- The Screening Agent checks James’s profile against sanctions lists, PEP databases, adverse media sources, and internal watchlists.

- The Wealth and Funds Review Agent looks at James’s source of wealth and source of funds. It reviews the business sale documents, bank statements, and crypto-related records to see whether the source of funds explanation is supported by the documents.

-

The Business Structure Review Agent checks whether James was connected to the business that was sold. It may look at business registration records, ownership records, or sale documents to check whether James’s business sale supports what he declared.

The business sale review is done by the Business Structure Review Agent. I covered it briefly in the Wealth and Funds Review Agent article only to make James’s full $5 million transfer easier to follow.

- The Signal Aggregator takes the separate findings from the individual agents and converts them into one unified input for the Risk Engine. This step is needed because each agent may produce output in a different format, and the Risk Engine needs a clean structure to apply its rules.

- The Risk Engine applies rules to decide what should happen next with the case. It does not just say ‘high risk’ or ‘medium risk.’ It explains why and which issues need human review. This decision is rules-based, not made by an AI model, because the bank needs to explain which rules were applied to regulators. The LLM takes the structured Risk Engine output and turns it into plain English. It writes a case summary that explains what was verified, what remains unresolved, and where the compliance officer should focus their attention.

- A qualified compliance officer reads the summary, reviews the unresolved issues, examines the supporting evidence, and makes the final decision. They can approve the case, reject it, request more information from James, or escalate it to senior management.

- The final layer records two things: the case record and the agent trace. The case record captures client information, review outputs, and the final decision. The agent trace captures which steps ran and where the workflow paused.

That is the architecture at a high level.

In upcoming posts, I will dive deep into each part of this workflow and explain how each layer works.

How this workflow reduces onboarding time

The workflow reduces onboarding time in three ways.

First, simple cases move faster.

Not every high-net-worth client needs deep scrutiny. If a client has straightforward wealth from a high salary, no PEP exposure, no sanctions concerns, and no complex business structures, the Orchestrator skips unnecessary steps. Clients with clean profiles can be reviewed and decided in days instead of weeks.

Second, complex cases reach the right compliance team earlier.

Cases with PEP exposure, crypto funds, business sales, or trust structures need special attention. In a manual process, someone reads 50 pages, discovers the crypto issue buried in the statements, and routes it to someone else who starts over.

In an agentic workflow, the Orchestrator spots these issues early and routes the case immediately. The compliance officer sees what is supported, what is unresolved, and where to focus. They can spot-check the evidence and decide quickly.

Third, cases pause and resume without losing context.

KYC cases pause constantly. A document might be blurry and needs resubmission. A screening match needs verification. A transaction needs more documentation.

The Workflow Controller records where the case paused and what needs to happen next. For example, when James submits the missing document, the case resumes exactly where it stopped. The compliance officer continues without starting over.

What this workflow actually does

This workflow does not approve clients. The compliance officer still makes that decision.

It also does not replace the systems banks already use for identity verification, sanctions screening, document storage, case management, or human review. Instead, it connects to those systems, collects their outputs, and organizes the results into a cleaner format for the compliance team.

That is where the real value is.

The relationship manager gets a clearer view of what information is needed from the client. The compliance team receives a better-prepared case. The compliance officer can focus on the unresolved issues instead of searching through the entire file. And if the case is reviewed later, the bank can explain what happened because the key steps were recorded together.

So the goal is not to replace the bank’s KYC process.

The goal is to make that process faster, cleaner, and easier to review later.

Let’s quickly recap

We started with James, a retired business owner who expected a premium onboarding experience but faced a 40-day wait because of a fragmented KYC process.

The solution is a workflow that routes the case correctly, runs specialist agents in parallel, organizes the findings, applies rules, and gives the compliance officer the right evidence faster.

That is how agentic AI becomes useful in KYC. It does not replace compliance officers. It prepares cases that are cleaner, faster to review, and easier to audit.

The goal is to help the compliance officer review the right case with the right evidence, faster.

That is how you reduce high-net-worth client onboarding time with an agentic KYC workflow.

The next post will go one step earlier in the workflow and show how CRM inputs, uploaded documents, and client declarations become the case package that the Workflow Controller uses to start the KYC process.

Stay tuned.